IN A FALLING RATE ENVIRONMENT, WHERE EASY MONETARY POLICY LOOKS SET TO PERSIST FOR THE FORESEEABLE FUTURE, INVESTOR DEMAND FOR FIXED INCOME INVESTMENTS OFFERING AN ATTRACTIVE YIELD WILL LIKELY INCREASE. HOWEVER, A BENCHMARKED APPROACH TO HIGH YIELD MAY NOT BE IDEAL FOR MANY INCOME-ORIENTED INVESTORS. ALTERNATIVELY, A MORE DEFENSIVE APPROACH THAT FOCUSES ON THE SHORTER END OF THE HIGH YIELD MARKET MAY OFFER A COMPELLING SOLUTION, RETAINING THE POTENTIAL FOR HIGHER RETURNS BUT WITH LOWER EXPECTED VOLATILITY. By Ulrich Gerhard and Cathy Braganza

THE APPEAL OF HIGH YIELD CREDIT IN THE CURRENT ENVIRONMENT

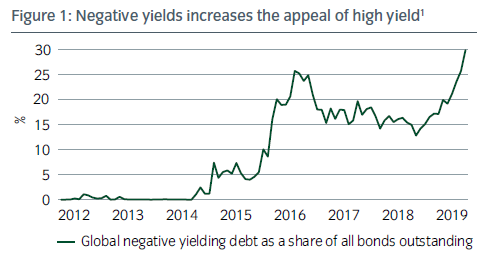

A glut of low and negative yields We are in a world where attractive yield opportunities are increasingly difficult to come by. This is a falling-rate environment where easy monetary policy looks set to persist for the foreseeable future, and where 30% of the global bond stock has a negative yield (Figure 1). This backdrop should underpin investor demand for fixed income investments offering an attractive yield.

More yield, low defaults

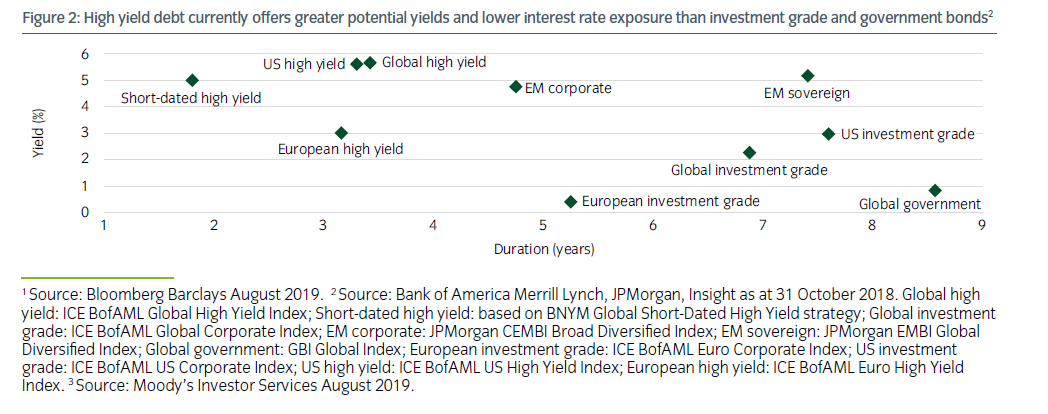

High yield debt is well positioned to attract much of this investor demand. In terms of yield, the asset class offers an average between 3% and 6%, depending on currency, which compares favourably with the 0 to 3% available from investment grade markets and the below 1% available from government bond markets (Figure 2). Of course these government and investment grade average yields mask a vast universe of sub-zero yielding European debt.

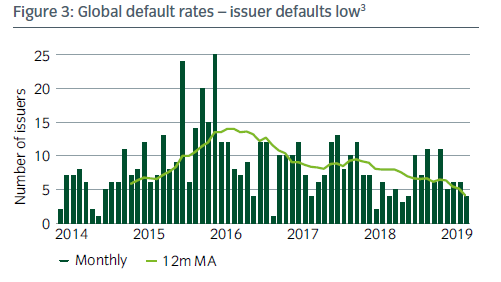

While global default rates currently remain very low (Figure 3), the low interest rate environment gives rise to increased concerns about rising leverage and the potential for defaults further down the line. This is balanced however by the low cost of financing. With interest rates so low, debt affordability has never been better.

Proactive refinancing management

Companies in the high yield space have been proactively managing their refinancing needs by both making sure they issue replacement bonds when markets are most receptive to buying new issues and also securing refinancing well ahead of need to ensure there are no liquidity gaps. Furthermore, high yield issuers have become increasingly flexible in their willingness to adjust the maturity of new issues to suit investor preferences. We have therefore seen a wide variety of both longer- and shorter-dated bonds being issued.

A strong technical backdrop

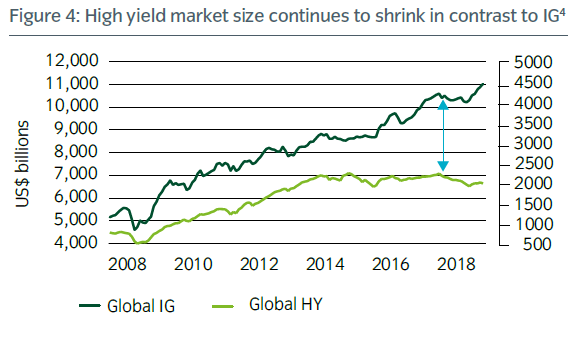

Lastly the technical background for high yield remains strong as the market continues to shrink relative to the IG market (Figure 4). Current new issuance volumes only just about match redemption amounts, meaning that any additional demand for high yield credit coming from investment grade credit investors will likely push prices up.

POTENTIAL DRAWBACKS OF HIGH YIELD

Despite improving fundamentals, high yield investing comes with certain risks. Within high yield indices are companies with very poor fundamentals and unacceptably high levels of default risk. Approximately 16% of the global high yield index consists of issuers with a rating in the “C” rated buckets, and these credits have a 5-year cumulative loss rate of 20.5% according to Moody’s. At Insight, we tend not to invest in issuers with a senior credit rating below B-.

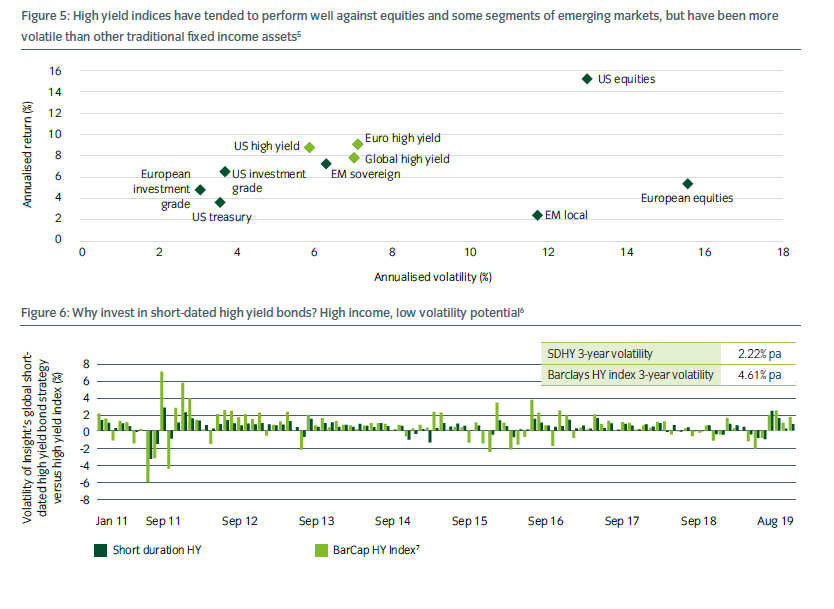

Given the potential for higher default losses, high yield indices generally tend to be more volatile than investment grade and government bond indices, although compare favourably with equities and some segments of the emerging market debt complex (Figure 5). Short dated high yield enjoys comparatively lower volatility than broad-index high yield, owing to its shorter duration profile (Figure 6).

REDUCING VOLATILITY THROUGH SHORT-DATED HIGH YIELD

For investors seeking a higher yield, but with lower volatility, a shortdated

approach can be more defensive than a broad-benchmarked high

yield strategy. This is largely due to the ‘pull to par’ phenomenon.

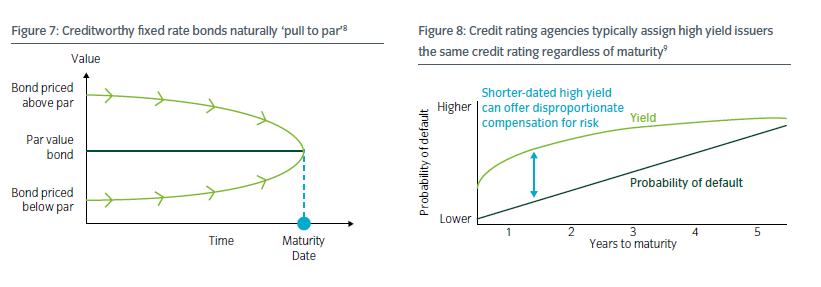

Provided credit quality has not been impaired, the closer the bond gets to maturity, the more certain it is to redeem at 100% of its par value. Therefore, over time, the bonds will naturally ‘pull to par’ (see Figure 7) – whereby a fixed rate bond gravitates towards par over time whether trading at a premium or discount, assuming no impairment. With a good understanding of the company’s liquidity position it can be remarkably clear whether the issuer will be able to meet its most imminent debt obligations. For longer-dated assets, such analysis becomes progressively more challenging given the many macroeconomic and microeconomic variables at play.

Therefore, short-dated bonds are fundamentally less susceptible to changing interest rates and average credit spreads. Furthermore, debt frequently matures in short-dated portfolios, generating cash. Should yields or credit spreads rise, cash can be reinvested at higher rates to further smooth the impact of volatility.

Fortsetzung nächste Seite