It is notable that several companies issue debt in both euros and US dollars, and their bonds can trade differently in each market, providing relative value opportunities. Diverging global monetary policy contributes significantly to this. The euro high yield market, for example, has been indirectly influenced by the European Central Bank’s investment grade corporate bond purchase initiative. But as no equivalent program exists in the US, pricing dynamics differ. With too few managers investing across both markets, these inefficiencies and pricing differences will likely persist. Divergence in pricing (see Figure 10) also illustrates the benefits of diversification. The US dollar market has a larger proportion of single-B issuers, while the European single-Bs are significantly weighted toward peripheral Europe.

SUCCESSFULLY INVESTING IN SHORT-DATED HIGH YIELD

High yield is a specialist investment area and demands substantial skill and resources. As defaults can inflict substantial losses, a focus on bottom-up credit analysis is required. We believe analysts need to focus on the areas highlighted in Figure 11. Understanding a business profile requires a strengths, weaknesses, opportunities and threats (SWOT) analysis and a competitor review. High yield companies often have investment grade peers, an ideal yardstick for financial comparisons. This demands credit coverage across all markets. Free cash flow can also be an important determinant of the issuer’s financial viability.

The ability of the company to call (redeem early) or not call ist bond can also directly impact its value. The terms and conditions regarding a high yield bond can be complicated and term sheets are frequently several hundreds of pages long. They include details regarding structural protections such as seniority (the bond’s priority in the capital structure), security against company assets and debt covenants. The latter can help ensure a bond’s credit quality is not compromised by company management. Structural protections do not typically apply to investment grade bonds.

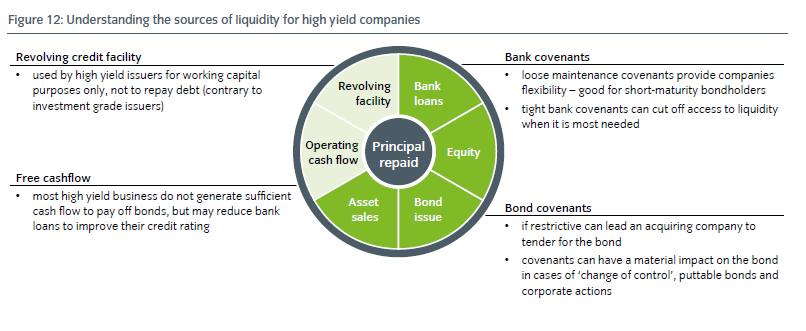

The sources of a company’s liquidity (see Figure 12) are a crucial determinant of its ability to repay. When investment grade companies have no cash available to repay the bond’s principal they can usually draw on a revolving credit facility. However, high yield companies will not typically have a facility that is large enough. Furthermore, for high yield companies the facility is typically secured against inventories, further blocking available sources of liquidity. It also typically comes with debt covenants that can further restrict the issuer’s available liquidity. Similarly, the issuer’s bank or bond covenants can also be restrictive. High yield companies without enough available liquidity may need to revert to asset sales as a last measure, but this would not be sustainable. In a worst-case default scenario, the issuer’s debt will be restructured. Investors with the practical and legal understanding of the restructuring process will be best placed to ensure the best recovery rates on the bonds.

CONCLUSION: STABLE INCOME IN AN UNSTABLE ENVIRONMENT

High yield markets are typically vulnerable to default rates. Default rates are currently low and look set to remain benign over the coming year. However, volatility is inevitable in a world where monetary policy has entered unchartered territory and global politics are increasingly uncertain. Prudent investors seeking income rather than growth through high yield bonds should adopt a considered approach to risk, backed-up by a rigorous, analytical and diverse investment approach.