By Steven Oh, CFA, Global Head of Credit and Fixed Income, PineBridge Investments, Los Angeles

- It’s not likely the conditions of 2019 will be repeated, where safe-haven government bonds as well as higher risk fixed income assets performed well.

- We expect 2020 to be marked by a continuation of bifurcated risk appetites, in which many investors steer clear of the highest risk segments within assets, mainly due to concerns about deteriorating credit quality amidst a late cycle environment.

- While we forecast lower growth and lower returns for 2020, we don’t foresee recession.

As the global economy settles into a lower growth trajectory, central banks are reengaging in the next phase of stimulus following a short and largely unsuccessful effort at policy normalization. The return to monetary easing in 2019 resulted in an unusual outcome of synchronized positive returns across asset classes. Yields on safe-haven government bonds plunged as recession concerns surfaced across developed markets, yet credit-risk assets also performed well due to the ongoing thirst for yield and the belief that pre-emptive actions by central banks would prevent recession.

Recently, a shift has been taking place, and appetite for risk has become increasingly bifurcated. There is growing aversion to the highest risk segments and to earnings disappointments, creating rising dispersion within asset classes. Overall, credit fundamentals have declined, the industrial sector has been slowing, and slack investment spending has been discouraged even more by uncertainty arising from ongoing trade tensions. Consumer strength and robust employment should counter these negatives and mitigate recession risks.

What lies ahead for 2020, therefore, is an environment of lower global growth matched with low yields and much lower returns, yet increasing opportunities for security selection alpha.

Six trends to watch

We believe the following trends will shape the fixed income investment environment in 2020:

1.Central bank detente. Developed market central banks reversed course in 2019 and engaged in additional stimulus. The European Central Bank (ECB) reintroduced its asset purchases, along with a rate cut, while the Federal Reserve (the Fed) enacted its ‘mid-cycle’ adjustment of three 25-basis-point rate cuts. The Bank of Japan (BOJ) has acknowledged the counterproductive effects of negative interest rates and appears to be determined to utilize other methods for its monetary policy tools; the ECB is also hitting its lower bounds and has limited options. Despite concerns relating to economic weakness and absence of inflation, we believe central banks would prefer to refrain from any additional rate cuts as long as currency levels remain stable and political risks are kept in check.

Following its three cuts, the Fed appears to be setting a higher threshold for 2020 in terms of cuts or hikes, with a strong bias to maintain current levels. This sets the stage for government bond rates in developed markets to remain range-bound for 2020, but with tail risks that are primarily political and policyrelated, tilted toward the downside. In the US, tail scenario odds favor rates going lower rather than higher, despite the fact that fundamental fair value would dictate a somewhat higher rate outcome.

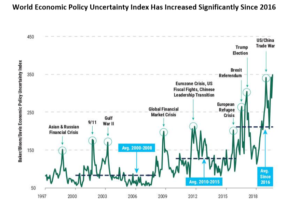

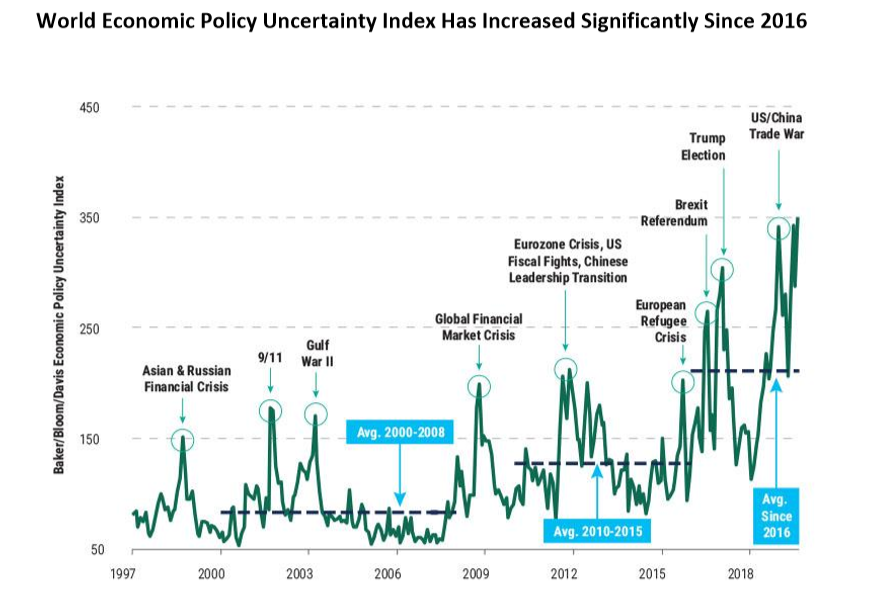

2.Ongoing political risk. The most significant headwind to the global economy has been the escalation of trade tensions and the myriad of political risks that are regional or country-specific. While both the worst case scenarios for US-China trade and Brexit appears to be tempered for the time being, political risks will linger in 2020 and have the potential to quickly shift investor sentiment. This uncertainty will dampen capital investment. In the UK, the ongoing Brexit limbo may finally end with some kind of agreement in early 2020, but probably not without more political turmoil.

And, of course, the US presidential election in 2020 could result in material changes in policies. Rising discontent in developed countries stemming from income inequality is leading to more populist governments and nationalism, which fuels protectionist policies that hinder global trade. This is a trend that is unfortunately likely to continue, irrespective of which parties emerge victorious.

3.More favorable fundamentals in emerging markets. In contrast to slowing growth and earnings across developed markets, many emerging market (EM) economies are exhibiting improving fundamentals. While some EM problem cases, such as Argentina, generate headlines, these are idiosyncratic blow ups that are 2020 Fixed Income Outlook | 3 self-contained and pose minimal largescale risks. Moreover, we see improving economies, lower inflation and stable currencies in many EM countries and regions, which will allow for central banks to lower interest rates and provide support for fixed income investments.

4.Rising dispersion and security selection opportunities. For the past several years, markets have been largely operating in a beta market shaped by near term risk-sentiment. The second half of 2019 has been marked by a significant increase in dispersion within credit assets. This dispersion and market bifurcation is resulting in greater security selection opportunities and potential for future alpha returns for credit pickers who can correctly identify the undervalued securities within a fair, to somewhat overvalued, market.

5.Out of favor segments have value potential. A contrarian philosophy of seeking opportunities where valuations have improved due to investor aversion creates risks, as well as potential for alpha returns. When this value gap is a result of technical conditions, rather than fundamental underpinnings, the risk-adjusted returns become more attractive. The demand aversion to floating rate credit in 2019 as interest rates declined has resulted in attractive opportunities within this space, particularly in segments of the secured loan market and in mezzanine tranches of collateralized loan obligations (CLOs).

6.Selectively adding risk. In 2019, our outlook recommended selectively derisking portfolios, particularly in the highest risk segments within asset classes. But as we head into 2020, with increased dispersion and a combination of significant demand for ‘higher quality’ credit and aversion toward ‘higher risk’ segments, relative value is tilting toward selectively adding risk in portfolios but with ongoing caution. In developed market investment grade (IG) credit, concerns relating to a potential mass downgrade of the burgeoning higher risk BBB segment is resulting in relatively attractive valuations. But this also can be viewed as a defensive allocation in relation to BB-rated high yield (HY) credits that are trading at extremely tight levels with unfavorable convexity.

Where the best opportunities may lie

Across leveraged finance, we see the best security selection opportunities in the mid-single-B space; we continue to maintain an underweight in the highest risk CCCs. We continue to favor secured loans over unsecured bonds, although risk profiles must be adjusted to reflect the quality shifts in both asset classes in recent years. And since cyclical industrial credits have underperformed, there will be opportunities to add exposure there selectively in 2020.

In contrast to developed markets, in emerging markets we see better riskadjusted returns in many high yield, rather than investment grade, securities. This shift is in contrast to 2019 when we advocated for portfolio exposures that were more heavily weighted toward IG.

The bottom line for 2020

Following a near ideal year for asset returns across the fixed income spectrum in 2019 (assuming no shocks in the year’s waning weeks), we are poised for substantially lower beta returns in 2020. However, our base case economic outlook of low growth, low inflation, and no recession is supportive of credit spread assets.

Steven Oh

Our forecast also calls for global corporate defaults to persist at low, below historic-average rates, but these should rise from 2019 levels to those which are closer to longer term trends. In an environment of declining beta returns with much higher dispersion, security selection alpha should have a greater impact on portfolio performance.